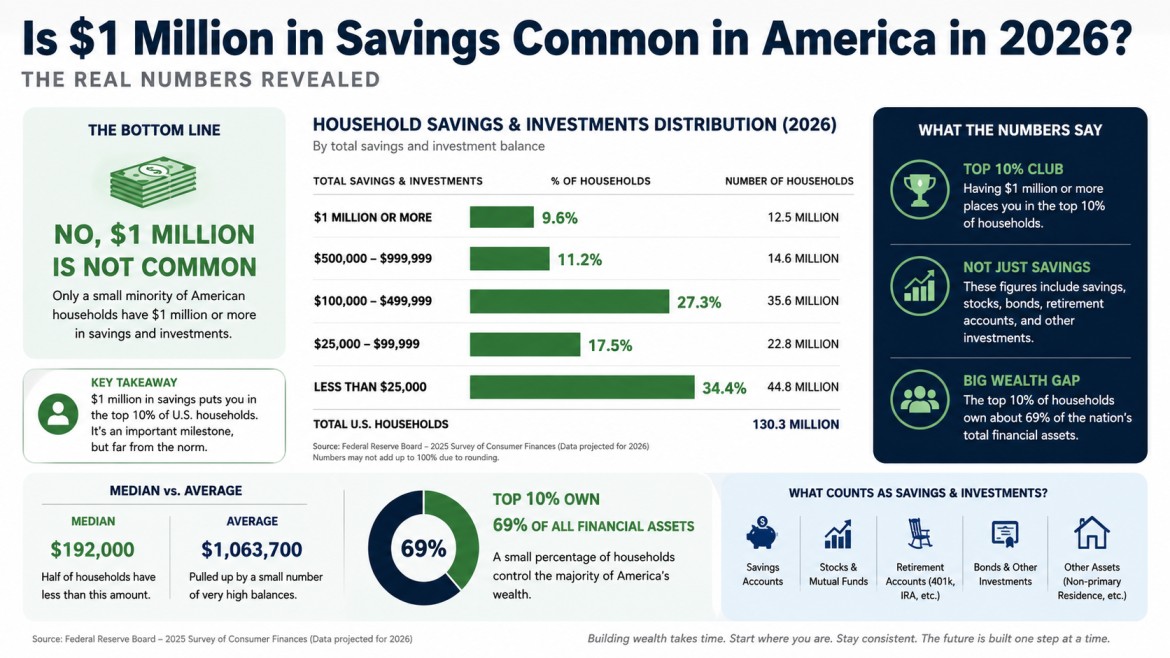

Having $1,000,000 in savings is a major financial milestone — but it’s far rarer than most people assume. In 2026, only a small percentage of Americans have reached this level when focusing strictly on liquid or investable savings (cash, bank accounts, stocks, bonds, retirement accounts — excluding home equity).

This comprehensive guide breaks down the latest data, distinctions between savings types, who achieves it, and practical insights for building your own million-dollar savings.

Key Distinctions: What Counts as “$1 Million in Savings”?

“Savings” can mean different things:

- Retirement savings (401(k), IRA, etc.): Strictest and most common interpretation for “savings.”

- Liquid / Investable assets: Cash + investments (excluding primary residence) — the definition used for High-Net-Worth Individuals (HNWIs).

- Total net worth: Includes home equity, businesses, etc. (much broader).

The numbers vary dramatically depending on the definition.

Current Statistics: How Many Americans Have $1 Million in Savings?

Retirement Accounts Only:

- Only ~2.5% of all Americans have $1 million or more in retirement accounts.

- Among retirees: Just 3.2% have $1M+ in retirement savings.

- About 4.7% of Americans with retirement accounts have reached the $1M mark.

Liquid / Investable Assets ($1M+ excluding primary home):

- Approximately 6.8 to 7.9 million individuals in the US qualify as HNWIs.

- This represents roughly 2–3% of the adult population or about 1 in 40–50 adults.

Total Net Worth Context (for comparison):

- ~24 million Americans have $1M+ total net worth (including home equity) — about 8.8% of adults.

Wealth Distribution Table (2026 Estimates)

| Category | Number of People/Households | Percentage of Adults | Source Notes |

|---|---|---|---|

| $1M+ in Retirement Accounts | ~6–8 million | 2.5–4.7% | Federal Reserve SCF |

| $1M+ Liquid/Investable Assets | 6.8–7.9 million | ~2.5–3% | Capgemini / Henley |

| $1M+ Total Net Worth | ~24 million | 8.8% | UBS / Federal Reserve |

| Top 5% Net Worth (~$3.8M+) | ~6.5–7 million households | 5% | Various |

Who Has $1 Million in Savings?

Demographics:

- Age: Vast majority are 50–70+ years old. Wealth compounds over decades.

- Education: Over 85–90% have college degrees or higher.

- Background: Mostly self-made through consistent high savings rates, career growth, entrepreneurship, and investing.

- Professions: Tech, finance, medicine, law, engineering, and successful small business owners dominate.

Important Reality Check:

- Many with $1M in retirement accounts still have modest lifestyles because the money is not easily accessible until retirement age.

- Home equity inflates total net worth numbers but doesn’t provide daily “savings” liquidity.

Why So Few People Reach $1M in Savings?

- Low savings rates: Many Americans live paycheck-to-paycheck or save less than 5–10% of income.

- Late starts: Compound interest needs time (20–40 years).

- High expenses: Housing, healthcare, education, and lifestyle inflation.

- Market volatility: Even strong investors face drawdowns.

- Debt: Student loans, credit cards, and mortgages slow progress.

Positive Trend: The number of people with $1M+ in liquid assets has grown significantly (up ~78% over the past decade) thanks to strong stock markets and entrepreneurship.

How to Build $1 Million in Savings: A Realistic Plan

Reaching $1M is achievable with discipline:

- Start Early — Time is your biggest asset.

- Save Aggressively — Aim for 15–25%+ of income.

- Maximize Tax-Advantaged Accounts — 401(k), IRA, Roth IRA, HSA.

- Invest Wisely — Low-cost index funds targeting 7–10% average returns.

- Increase Earnings — Side hustles, career advancement, business ownership.

- Avoid Lifestyle Creep — Live below your means.

- Automate Everything — Pay yourself first.

Example Timeline:

- Saving $1,500/month at 8% annual return starting at age 25 → $1M by mid-50s.

- Higher income or later start requires larger monthly contributions.

Challenges of Having $1M in Savings

- Inflation: Erodes purchasing power over time.

- Taxes: Withdrawals from traditional accounts are taxable.

- Healthcare Costs: Major risk in retirement.

- Sequence Risk: Bad market timing early in retirement.

- Not Feeling Rich: In high-cost areas, $1M may support a comfortable but not luxurious life.

Myths About $1 Million in Savings

- Myth: It’s easy or common. Fact: Only a small elite percentage achieve it in liquid form.

- Myth: You need a huge salary. Fact: Consistent saving and time matter more.

- Myth: $1M guarantees a stress-free retirement. Fact: Depends on lifestyle and location (many target $2M+).

- Myth: Most inheriting it. Fact: Vast majority are self-made.

The Future Outlook

With continued market growth, technological opportunities, and the Great Wealth Transfer, more Americans will reach this milestone. However, rising costs may require higher targets for true financial independence.

Frequently Asked Questions (FAQ)

How many Americans have $1 million in savings in 2026? Approximately 6.8–7.9 million have $1M+ in liquid/investable assets. Only ~2.5% have this in retirement accounts specifically.

What percentage of Americans have $1M saved? Roughly 2.5–3% for liquid assets; 8–9% when including home equity in net worth.

Is $1 million enough for retirement? It can be in lower-cost areas with modest lifestyles, but many financial planners recommend $1.5M–$2M+ for security.

How rare is $1M in the bank? Extremely rare. Most “savings” at this level are invested, not sitting in cash.

Can average earners reach $1M in savings? Yes — through decades of consistent investing, compound growth, and avoiding debt.

What’s the difference between savings and net worth? Savings/liquid assets are accessible money; net worth includes illiquid assets like your home.

Conclusion: $1 Million Savings Is Rare — But Achievable

In 2026, having $1 million in savings puts you in an elite group — roughly the top 2–3% for liquid assets. It represents serious financial discipline and long-term thinking that most Americans never achieve.

The good news? The path is clear and available to anyone willing to start today: save consistently, invest wisely, and let time work in your favor.

Whether you’re starting from zero or already building momentum, every extra dollar saved and invested brings you closer to this life-changing milestone. Track your progress monthly, adjust as needed, and stay committed.

True wealth is built one smart decision at a time.

This article is for informational and educational purposes only. Consult qualified financial advisors for personalized advice. Data based on Federal Reserve Survey of Consumer Finances, Capgemini World Wealth Report 2025, Henley & Partners, and other reputable 2025–2026 sources.

Agnesa Brinkmann is a senior writer at LA Magazine with over 4 years of experience interviewing entrepreneurs and business owners from all around the world.